The Changing face of Debt in Canada

Debt in Canada has changed dramatically over the past fifty years, and not for the better. If you are as old as I am you may very well remember when it was a requirement of using revolving credit that it revolve periodically. Revolving of course meaning that the debt gets paid in full, so your credit card or credit line balance would need to be reduced to zero or near zero from time to time.

The consequence of not revolving, revolving credit, would be a suspension of that credit card/line until it did revolve. Back in the day, minimum monthly payments were also higher than they are today, minimum monthly payments have become progressively smaller to the point that they are completely insufficient to reduce the principal amount of the debt.

Canadians have adapted to insidiously growing debt levels that have now reached a point of being irreconcilable without major regulatory changes to our banking system. Now, the (Anti) Competition Bureau is pushing the notion of unending, unpayable, debt to prevent the banks from facing utter collapse.

The basic idea being pushed is reflective of Modern Monetary Theory a rather old classroom idea put forward by economics students and professors. As with all economics theories, they are basically Ponzi type schemes designed to keep clients, banks and large corporations, from suffering the consequences of poor business decisions at the expense of the proletariat.

The data doesn’t lie, but the narratives and economic theories constantly shift. The only thing we can be completely certain of is that whatever direction the tide shifts towards will not benefit most of humanity, it will benefit the top, controlling oligarchs.

Now imagine a world in which you owe three times (3X) as much money as you earn, a world in which it is impossible to repay your debt, and in which it is impossible to live without access to new debt. Could you imagine that world? That is the world in which Canadians are already living.

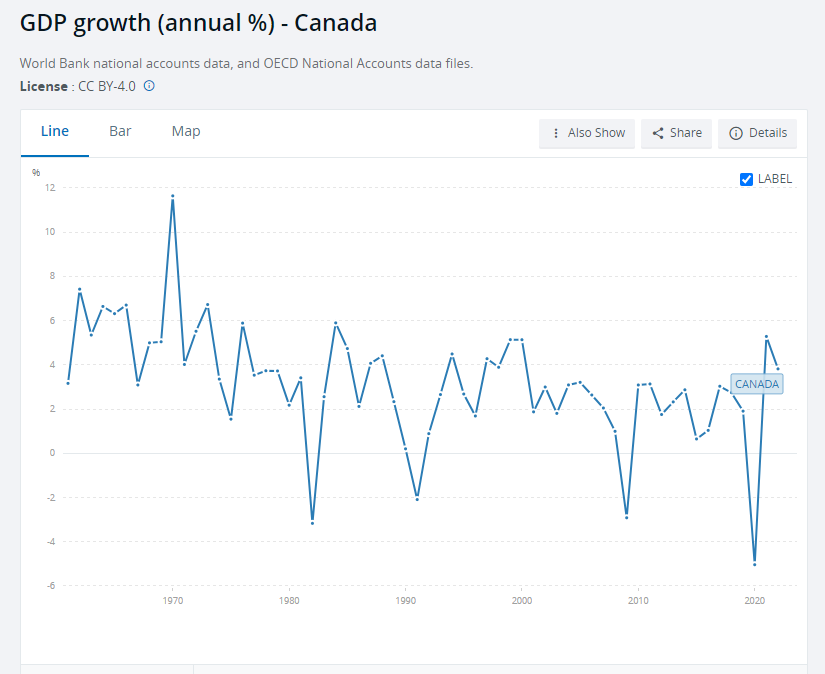

GDP in Canada is about $1.9 trillion and shrinking and has been in general decline for the past ten years. Meanwhile Consumer Debt (including mortgage debt) is about $4.3 trillion and doubling every three years. Average income in Canada dropped by 8.5% between 2019 and 2022.