Debt is Destructive

Debt is very destructive, it destroys peoples’ of lives, economies, societies, families, and certainly the so called middle class. Debt has always been around, in fact from the earliest times of bartering – “lend me a fish and I’ll owe you a loaf of bread“. But debt as we know it today is a relatively new phenomena.

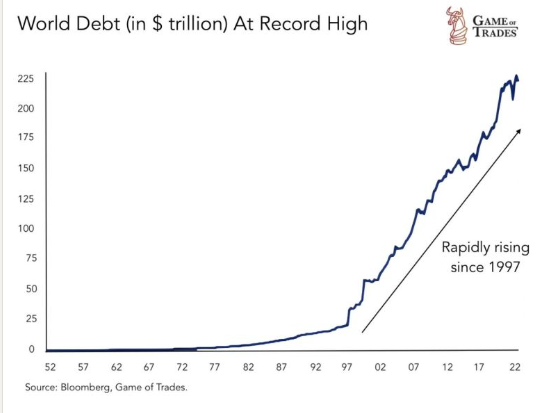

Modern debt really started in the 1970s and surged in the 1990s. Today, debt is so ubiquitous that very few Canadians can even afford to live without it. Canadians are the most in-debt consumers in the world. Interestingly, the well known British wealth inequality economist Gary Stevenson points out that debts a zero sum game – for every dollar borrowed there is a dollar owed.

However, only the very wealthy can afford to lend money, whether they lend it through investment portfolios or lend it directly. Banks of course have no money to lend, so they use clever accounting techniques to effectively create money out of thin air. At the end of the day, ordinary people are fooled into believing that having access to debt confers some form of benefit to them.

The absurdity of this contention must not be lost with recent bills being passed in Quebec and likely in the rest of Canada – spurred on in no small part by the Competition Bureau.

The reality is the only beneficiaries of debt are the lenders, never the borrowers. People use debt to take their family on vacation, then pay for the vacation for the next few years or even more – was it really worth it? Was there a benefit to an impulsive vacation that caused you to struggle to pay for groceries? Yes, very definitely, if you are the lender – where else can you earn a 21% return on your investment of money that was just sitting around?

If you did nothing else with your money but repay all your debt you could be debt free in 2-10 years. But how are you going to live? Who’s paying the mortgage (debt) or rent (someone else’s debt), much less groceries, transportation, etc.?

Canadians owe nearly $4 trillion in mortgage debt, according to one report, and about $2.16 trillion according to others. No matter how you view it, Canadian consumers are literally wallowing in unpayable debt. There is literally no path that exists for most Canadians be able to repay their debts in the ordinary course of business.

Inflation has been a hot button topic that is grossly misrepresented as reports of inflation calculations cherrypick the items that will be used in calculating measures. Using debt compounds the problems of rampant inflation by increasing the cost of everything purchased while using debt. Every single time you use debt you increase the cost of everything you purchase and you reduce the value of your paycheque.

We’ve said it before – “getting out of debt is easy” – we are just a phone call away. But, staying out of debt is a real challenge in the face of rampant inflation, especially in the face of an already over leveraged economic environment. What you can do, is slowly wean yourself off of debt, It will take years to stop using debt, to stop all superfluous spending – no more trips, meals outside of the home, walk more and drive less, do what you have to do to get your budget under control and rein in spending.

Budgets have three mechanisms for improvement, the first is to increase income, the second is decrease expenditures and the third is to a little of each of the first two.