Buying a House

Buying a house is simply not what it used to be, in 1981 the national average house price (in 2024 dollars) was $252,176. The reason I picked that year is because it also had the highest interest rates in recent history with a peak of 28% in August of that year.

What should be clear to all pundits is that today’s national average house prices ($707,100 in November 2024) are grossly overvalued. In fact, today houses are about 200% higher than where they should be to be in line with inflation and income levels.

Buying a house in today’s market is probably a fool’s errand, it is a sure way to impoverish yourself and your family. Don’t buy into the FOMO hype you can’t afford it, step back and look at the big picture.

If you buy a house for $707,100 with 20% down and have a mortgage at 5.2% your monthly payments (on the mortgage $565,680) would be $3,355 or a total of $1,006,500 assuming the rate never changed over a 25-year amortization.

You would also have paid the 20% downpayment so the total cost of your purchase would be $1,147,920 for a property that apparently should be priced at $252,176. Who benefits from your indebtedness? Certainly not you!

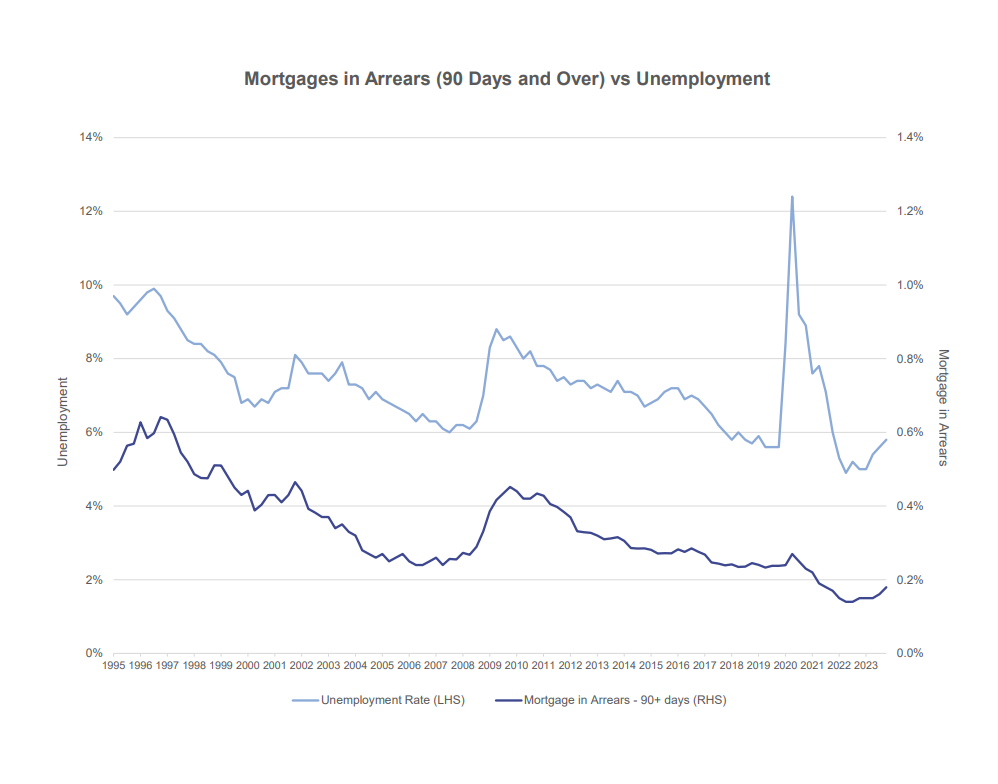

The current market trend suggests a correction is in progress with very high listing to sale ratios compared to the boom years of 2020-2022. The graph above, from the Canadian Bankers Association shows that since 2022 the number of mortgages in arrears has grown by close to 30%.

The graph also shows that official unemployment rates have grown over the same period by about 15% – however, this data needs to be viewed with extreme caution, most jobs created have been either direct government jobs or government subsidized jobs through temporary foreign worker programmes.

When the government hires workers or subsidizes their hire, the cost is passed on to the private sector in the form of taxation – so the apparent gains in GDP are really unsustainable and not helpful to the economy at large. When government workers pay taxes, they contribute nothing new to the economy.

Government subsidies rarely result in higher paying jobs as they tend to put downward pressure on incomes while increasing the tax burden. In this environment, very few people can afford to pay the massive costs associated with huge mortgages on overpriced properties.

In fact, even the often-touted Sunshine Listers are a dwindling population with less than 5% of those listed belonging on the list after adjusting for inflation. In any event only about 7% of Canadian taxpayers earn over $100,000 per year (before taxation).

Just today data was released by the media indicating that 25% of Canadians are living in poverty with many reliant on food banks. One might ask “is it reasonable to believe that house prices will increase in this economic environment?”. If the answer is “NO” then the best advice is to hurry up and wait before buying a house!