Mortgage Defaults on the Rise

Recent media reports indicate a 600% increase in Powers of Sale by banks, with private mortgagees also commencing similar proceedings. Other reports note that 1.4 million consumers are in arrears on debt payments.

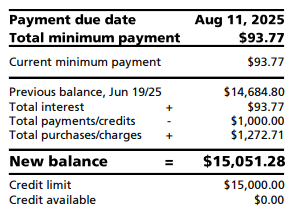

Defaults are inevitable in today’s debt-saturated economy. A significant percentage of the population is entirely debt-dependent, with no realistic hope of repaying their obligations—and lenders knew this when they extended the credit. Take, for example, the screenshot of a Bank of Nova Scotia (BNS) credit card statement, particularly the “minimum monthly payment” section.

To be clear, this is not unique to BNS. RBC, TD, BMO, and other major banks employ similar repayment schemes. Debt is Canada’s single largest industry, and for those on the lending side, it is also one of the most lucrative. CBC Marketplace has aired several exposés showing how banks manipulate the system to qualify people for debt they should never have been approved for. Yet, as so often happens, the victim is blamed more than the perpetrator.

Domestically, Canadian banks are often seen as paragons of integrity. A closer look, however, reveals a very different picture. Internationally, Canadian banks have gained a reputation for fraud and money laundering, a practice dubbed “Snow Washing.” Fraud is rampant in Canada and effectively sanctioned by regulators through willful blindness. Rather than address systemic issues, the problem is downplayed to preserve “trust in the regulators.”

In the U.S., TD Bank was fined $4 billion (CDN) for fraud and money laundering. In Canada, regulators imposed a mere $9 million in administrative penalties for similar offenses. Meanwhile, during the RCMP investigation into HSBC for fraud and money laundering, the bank was effectively “laundered” through RBC’s swift purchase—for the low price of $13.5 billion.

This raises the question: What are Canadian banks really worth? HSBC was reportedly the seventh-largest bank in Canada. Consider these figures:

- About $145 billion worth of Bank of Canada Bills are in circulation.

- As of December 2024, Canadians owed $2.4 trillion in mortgage debt.

- When all consumer and small business debt is included, the total reached $6.6 trillion.

Now consider the definition of a mortgage in arrears. In Canada, according to the Canadian Bankers Association, a mortgage is only in arrears if three or more monthly payments are overdue and not subject to a lender forbearance agreement. In most other countries, a single missed payment qualifies as arrears. This definition serves to obscure the true depth of mortgage defaults in Canada.

A troubling trend has also emerged: many Canadians are leveraging real property for additional debt through multi-layered mortgages, with some households carrying three or more encumbrances on their homes. The debt crisis in Canada is deepening, and the regulatory response has been wholly inadequate.