Post Christmas Debt

We are, predictably here again, singing the Post Christmas Debt Blues – it’s a lot like having a couple of extra drinks because you’re feeling good in the moment. It seems like a good idea at the time – but the hangover…

You justify excess spending your way, we all do it – whether “it’s for the kids” or “it only happens once a year” make up your own tag line, there are plenty to choose from. Excuse it how you will but spending on credit cards will have a consequence, and it will not be as much fun as Christmas.

Let’s talk strategy, first thing to do is sit down with the family (everyone impacted by your household expenditures) and build a household budget. Some expenses are easy to recall but some may need to be estimated based on either recollection or perhaps a copy of a bank statement.

The cost of living is always increasing; in recent years many common expenses have increased by 30-40%. This is called “inflation”- the Bank of Canada and, by extension, Parliament track inflation to help design policy. However, the measures they use exclude many important and volatile expenses such as transportation, housing, and groceries.

| ITEM | 1980 COST | 2026 *ADJUSTED COST | 2026 ACTUAL COST |

| House Price | $47,200 | $169,795 | $685,000 |

| New Vehicle | $7,574 | $27,233 | $64,000 |

| Bedroom Suite | $300 | $1,079 | $2,525 |

| Income | $26,700 | $96,004 | $74,000 |

In the matrix above we can see how far out the official data is from the reality of everyday life in Canada. Assuming the *inflation adjusted costs were aligned with real world data Canadians would be much better off than they are.

The extreme costs of living in Canada are driving people into debt first, and then into poverty at levels not seen before. The only reason we do not appear to be in the same shape as folks who lived through the Great Depression of 1929 is easy access to DEBT!

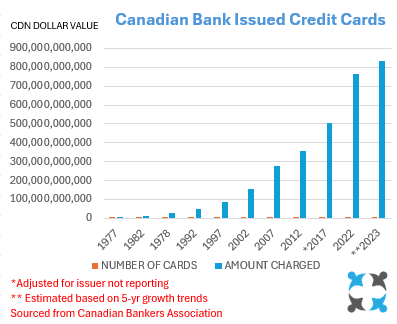

We have estimated that while 43% of our income disappears into some form of taxation, about 42% is being used to service debt. Canadians carry more consumer debt than any other people in the world, in fact we charge more on credit cards each year than we earn in after tax income. Our total consumer debt load is approximately three times the country’s GDP.

After examining your family budget if you find that your income is insufficient to cover all of your costs you need to consider the three options available to your and your family: 1. Increase Income, 2. Decrease Expenses, or 3. Do a little of each. When cutting expenses start with those that are not necessary – such as alcohol, recreational drugs, tobacco, eating out, entertainment, gifts, etc.

Using an insolvency proceeding to reduce or eliminate debt is a short-term strategy that can be utilized to bring a debtor back to a new starting position. The problem, as we can see, is that debt becomes readily available – far too quickly – and debtors quickly find themselves gasping for relief, again.

Living costs can only be cut so far, and there are not enough hours in the day to earn enough income to sustain what used to be considered a normal average Canadian lifestyle.