Real Debt Relief – Caveat Emptor.

It is extremely challenging for Canadians to find “real debt relief”, not because we don’t want to but simply because real debt relief requires a systemic change and there is little or no political will to make the changes required. The origins of our consumer debt problems are multi-faceted and very complex; solutions require significant legislative changes that are unlikely to happen any time soon.

Problems with the Banks.

Canada’s consumer debt challenges began in the late 1970s and are predicated largely upon deregulation of the financial industry. Deregulation accelerated during the “Little Bang” in 1987 notionally removing barriers between banking, insurance, and securities, allowing diversification, entry for foreign firms, and increased competition.

However, deregulation had the opposite effect of providing a competitive market space, and actually encouraged the growth of banking cartels and monopolistic behaviour. Canada’s banking industry has become a global leader in malfeasant behaviour. When we examine the top ten shareholders of each Canadian bank we find an incestuous relationship wherein bank subsidiaries and private equities first are the main shareholders – fluffing each others’ value.

Some of the more noteworthy instances of questionable behaviour includes HSBC being investigated the RCMP and swiftly purchased by RBC in what has the optics of being a coverup to halt further investigations which may have implicated other banks. Sam Cooper’s book “Willful Blindness” is very suggestive of this being the intended outcome.

The TD money laundering case in the USA has also been well reported, with TD Bank agreeing to pay about $4 billion (CDN) in a non-prosecution agreement to protect the bank’s executives from the possibility of serious penalties that may have included jail.

But even that didn’t stop them, according to a Department of Justice Official, a former TD Bank employee processed bank cheques in a money laundering network totalling at least some $128 million (CDN).

The problem, at bottom, is that no one is watching the watchers, deregulation gave the bankers far too much power and the virtually unchecked ability to do whatever they want to maximize profits on all levels of business. The banks regulate themselves by lobbying parliament and using fear tactics – such as the notion they are “too big to fail” so no matter how badly they screw up we, taxpayers, must always be prepared to bail them out – at times to the tune of more than a hundred billion dollars.

The average consumer is completely oblivious to the questionable behaviour of Canadian banks, even though the CBC has reported quite extensively on how we are all being manipulated into acquiring more debt than we can afford to repay.

Nonetheless, it is important for people what banks are and are not – banks are privately held corporations that are in the business of generating dividends for shareholders (themselves). They are not institutions that are dedicated to consumer protectionism, albeit they must follow government regulations, such as they are, as well as rules established by international central banking cartels.

Insolvency Solutions are Not Permanent.

Real debt relief cannot be found by filing either a bankruptcy or a proposal, these tools only provide temporary relief, they cannot do more. Insolvency processes are designed only to help with the issues that are present at the time the insolvency is filed. But those issues are not fixed in time – even though the legislation assumes they are.

Once a bankruptcy or proposal is completed the same banks are ready to pounce on the freshly cleansed consumer to fill their pockets with more debt instruments. From credit cards to personal loans, overdraft protection, HELOCS and so on – these debt instruments provide not only the bread and butter for banks but also put gravy on their plates.

Today, many bankrupts have access to new credit cards before they even get a discharge, and the cycle of debt continues.

Sadly, Canada’s economy is so bad that few consumers can earn enough money to survive without access to debt. Since the 1980s multi layered mortgages became a tremendous source of profit for the banks allowing them to mitigate lending risks by effectively stuffing their pockets with the only tangible assets that most middle-class Canadians are ever likely to own.

Because the entire Canadian Canadian economy is extremely debt dependent, to the point that for the majority of the population the cost of living is completely unaffordable without access to debt, even a discharge from bankruptcy cannot provide more than a temporary solution. The often touted middle-class used be precisely that – median Canadian income earners were the middle-class.

When we are told the middle-class is “shrinking” that is a reference to people who self-identify as middle-class. According to Google:

“The Organization for Economic Co-operation and Development (OECD) defines the middle class as any household earning between 75% and 200% of the national median after-tax income.“

When we use the OECD criteria we find a very different story, the middle-class isn’t “shrinking” it is “disappearing” entirely. It has been reported that government workers are paid about 32% more than comparable private sector employees – yet as we can see below in the section on “Creating Favourable Statistics” even they are falling behind year over year.

The point being that even after divesting ourselves of debt, incomes have lagged so far behind real living costs that in an effort to maintain what is perceived as a middle-class lifestyle (the lifestyle we used to enjoy) unsustainable debt is necessary, not optional.

Debt Saturation

After saturating the market with credit cards, the banks started to make unsecured lines of credit available creating the impression that consumers had more access to lower interest debt instruments. But the real purpose was to allow self-consolidation, by transferring higher interest (21%) credit card balances to lower interest (9%) lines of credit.

By allowing the washing of the credit cards through a self-structured consolidation, under the guise of interest relief, consumers were encouraged to extend themselves further on their credit cards. Running up even more debt with the illusion they still had money to spend.

As the consumer market became more and more saturated with debt the banks risked more defaults so other strategies needed to be implemented. Undoubtedly “some banker got a big fat bonus” for coming up with the idea of “reducing minimum monthly payments so low that it would literally take centuries to repay the debt”. We saw a CIBC credit card statement with minimum monthly payments calculated over a term of 420 years – the bankers make their own rules!

As if the idea of “perpetual debt” (based on Modern Monetary Theory – take it easy bankers, it is only a “theory“) wasn’t enough they decided that “increasing credit limits” would also help prevent defaults. Other strategies included “no interest balance transfers”. This allowed for another version of debt washing; by moving a balance from one card to another with no interest charges for six months the consumer arguably had the opportunity to pay off their more rapidly.

Sneaky Sales Tactics.

However, the actual strategy of the credit card transfers was to wipe the debt from the existing credit cards in order that they may be reused. Banks originally offered only one credit card – for instance during the 1990s if you had said Scotia Bank I would have said “VISA” and if you said Bank of Montreal I would have said “MasterCard” – however, today Scotia Bank now offers its clients “VISA”, “MasterCard” and “AMEX”.

The banks would suggest this is because they want their clients to have “options” but that is simply not the case, it has more to do with “monopolistic strategies”. By allowing you access to multiple credit card offerings you are less likely to take your business to competitors and the bank is able to profit from each card while you can use one to make payments on another all the while “avoiding default”.

Scotia Bank was one of the first banks to bring multi layered debt to expanded mortgage offerings, which was used to block the borrower from leveraging their home equity through competitors. Their innovative programme is called a STEP mortgage. S T E P being an acronym for “Scotia Total Equity Plan”.

The programme is basically a crafty sales technique (now employed by most banks albeit under other names). The client is offered a very competitive rate for their mortgage but in exchange they must pledge the entirety of available equity in the property as security to the bank.

So, if your home is worth $750,000 and the mortgage is only $250,000 the bank will register a mortgage for $600,000 (80% of the total property value). This will allow them to offer access to other credit “products” (the vernacular is very important – it must sound comforting). If you described, more accurately, consumer debt “a debt vortex” it would be a lot harder to sell.

For example, you may take out a line of credit for $300,000 and credit cards totalling another $50,000 to in aggregate total the $600,000 registered. In fairness to the bank, they probably did “mention” what they were doing at the time of signing the documents. Usually, they don’t get into the weeds of how it works they just say, “by over-registering they can lend you more money without incurring legal fees”.

Few insolvent individuals have any idea they pledged their homes as security for more than just the mortgage, and the line of credit. In some cases, the bankers may not have had all the proper paperwork executed prior to enforcing their security, but the unsophisticated borrower, and even their counsel, maybe blissfully unaware of their real position.

A person I know was taking on one such mortgage and sought my advice, the situation was the property was valued at about $300,000 with existing financing of less than $200,000. The person was seeking a mortgage of slightly more than $200,000 which was to be used in part to pay out existing “unsecured debt“. The bank granted the mortgage but insisted it be permitted register $500,000 on the property. A further clause required the borrower agree to not seek any additional financing at any other institution. This behaviour is immoral and should be regulated, in my view.

Other home buyers will use a secured line of credit in place of a traditional mortgage with the belief that the property value will continue to increase during the period they are able to make interest only payments – apparently improving their monthly cash flow. In reality it isn’t that simple as the interest just keeps coming and the principle amount of the loan remains intact.

Migrant Exploitation.

The recent migrant phenomenon has been blamed for many of Canada’s financial woes, and ultimately domestic debt challenges – along with “Donald Trump and his tariff programmes”. However, few Canadians are able to see the broader economic picture. Mass migration was a tool used by the government to stimulate the economy by artificially inflating GDP numbers and boosting the bankers through a form of “quantitative easing“.

Foreign students pay triple the fees applied to domestic students in Canadian colleges and universities. They are also typically paying higher fees for housing either through on-campus residency, and meal plans, or shared off campus rentals. A complaint I heard from a senior professor at Western University (who shall remain unnamed for obvious reasons) is that students are now referred to as “clients“, and as long as they attend classes and pay their fees, there is an “expectation” they will receive their degrees.

Banks all have so called “Newcomer Programmes” – a debt trap created for people arriving from countries that have little or no access to consumer lending. Just for having an accent or a different skin colour they are offered “free banking” as well as a “Credit Card” with a $5,000 limit along with a $15,000 “Line of Credit” and easy access to mortgage facilities.

The only qualifying criteria is that they have been in Canada for “less than five years“. No credit check, no job, no problem! We know folks who have been employed by colleges and universities as “International Recruiters” in fact a whole industry has sprung up around recruiting people from other countries to attend Canadian post-secondary institutions.

Some migrants arrive on temporary work permits, with a portion reportedly pre-purchasing their jobs through offshore agencies some come on student visas and some as landed immigrants. The government’s official statistics are manipulated to obfuscate the sheer volume of people arriving in this country, disclosure is available, but you must dig deeper than just asking how many “immigrants“.

Rather than encouraging immigration from countries with advanced economies and more highly skilled individuals, the policy has been to economically exploit folks willing to accept lower wages and lower living standards. This topic was covered in an earlier blog that discussed labour shortages during the 1960s and early 1970s. This feeds into the corporatocracy so prevalent today.

Refugees are reportedly canvased by Canada’s Immigration Department which not only lends them money, with a promise of a great future, to acquire a plane ticket, to come to Canada, but also stuffs their pockets with money in the form of start-up funding and even provides an iPad as an incentive. We are all familiar with the iPad gifts at the bank for switching accounts or taking on mortgages – but most folks are unaware the government does the same thing, although the government denies this behaviour – we have had clients report that incentive was given to them.

A Google search found a Summary Table for 2022

| Category | Total Admissions / Holders |

| New Permanent Residents (Landed Immigrants) | 437,539 |

| Study Permit Holders (New) | 550,187 |

| Work Permit Holders (Total Unique) | 605,851 |

| Refugees (Admitted as Permanent Residents) | 75,330 |

| Asylum Claimants (New In-Canada Claims) | 91,710 |

Well over a million people enter the country each year and are entitled to the Bankers “Newcomer Programme” either immediately or within the ensuing five years, with similar numbers being repeated year over year.

Assuming each migrant took advantage of the generous credit offerings of $21,000 that would equate to up to $38 billion in new debt per year. If you understand fractional reserve banking that equates to many times that value of new debt being created by banks. The five-year time frame allows teenage arrivals to have easy access to debt as they come of age.

Creating Favourable Statistics.

By giving migrants easy access to debt, they are inclined to buy stuff, furniture, cars, houses, food and so on – this creates the great Canadian illusion that GDP (spending) is up – that is until one looks at the per capital numbers which show a very different picture a picture of economic decline. Many economists, especially those sponsored by governments and the financial industry don’t want you to look at per capital numbers.

The problem, they say, with per capital numbers is they incorporate lower income earners – precisely the fastest growing category in the Canadian economy – and these low income earners (about 70% of all income earners) put a drag on the top income earners – particularly the top 10% – making it appear as if they aren’t doing so well. The argument is both transparent and ridiculous.

The same tactics are used to report the CPI, many volatile expenses such as food, housing and transportation are excluded from CPI calculations – until fairly recently, clothing costs were estimated using the cost of material rather than the off the rack cost finished goods.

The top 10% of income earners in Canada earn in excess of about $125,000. The median income as noted above is about $42,000 and the average individual income is only around $54,000 down from $59,000 in 2019. According to the CRA in 2023 Canadians reported income totaling about $1.8 trillion, After doing the math, and extracting the top 10% of income earners as outliers the vast majority of Canadian income earners are at or below the median income.

The government and bank economists dupe you into believing your income is higher than it actually is – it does not benefit them to tell you that every year you become more and more debt dependent, Economists hate real numbers they live in a fantasy world of theoretical outcomes.

Economists who pointed at “family incomes”, because families earn more than individuals, have changed terms. Now, they use measures of “household income” because “households” include multi-generations as well as non-family contributors.

Our financial system is not just corrupted with greed; it is extremely complex and layered with obscure terminology and fine print. Just take a look at the residential standard mortgage terms. It is doubtful that when you signed your mortgage your lawyer explained the whole document to you – in fact some lawyers may not have even read the entire document themselves.

How then does a consumer wallowing in this vortex of debt finally break free and find real debt relief? The answer is surprisingly simple, but unlikely to ever happen – we need to regulate and break up the banks. Force them to return to banking, alone, selling off all their other business, not to other monopolies but to smaller competitive entities.

The same issue rings true throughout Canada’s entire financial system, consumer legislation could also rein in insurance companies, the real estate industry, mortgage brokers and agents, investment advisers, and others.

Bankruptcy Discharge Hearings.

Some bankrupts are required to attend a court hearing in order to obtain a discharge – during which they are required to explain to the judge how their insolvency occurred, what steps they took to deal with their financial situation and provide other information about their situation.

Imagine if lenders were also required to attend discharge hearings and explain to the judge the basis upon which they made so much debt available, frequently knowing that the bankrupt lacked the capacity make restitution at the time of lending.

The Corporate Environment.

Canada, in spite of it vastness and diverse resource base is not an attractive place to do business, the regulatory cost of having a presence in this country is extremely high regardless of industry. The government touts nonsense such as “VW and Stellantis are investing in building Battery Plants in Ontario” then it downplays the fact that taxpayers are footing the massive bill, laying out $30 billion dollars, adding full environmental indemnification and providing other incentives that aren’t ever available to Canadian small businesses.

Nonetheless, Stellantis is packing its proverbial bags and moving out. Canada does not have an auto industry, it negotiated that away decades under the Auto-Pact, in fact Canada has very little going for it except the Debt Industry – which is the biggest single industry in the country by far and away moving more money than any other. Battery plants aren’t the only examples of taxpayer incentivized corporations, there are many more.

One of the more low end yet absurdly ridiculous government incentives was the $12 million government donation to Loblaws to upgrade their fridges. Canada’s manufacturing is dominated by foreign companies that thrive on tax breaks, subsidies, grants and other incentives – in some cases the return to the domestic economy is in all likelihood less than the gifts given to keep them here.

Alberta’s filthy oil business stands as an example – for the most part the oil is extracted from tar sands, a costly and dirty process before the extracted product can be refined. Unlike oil from middle eastern countries that can be sent directly to refineries without massive tar tailings ponds being left as a catastrophic environmental mess for the taxpayers to clean up.

To be clear the scars to the countryside can be clearly seen from high altitudes and are the size of a small country.

“The environmental cost of cleaning Alberta’s tar sands tailings ponds involves massive, multi-billion dollar liabilities, with estimates ranging from tens to hundreds of billions (e.g., $28 billion to $130+ billion), but companies have only provisioned a tiny fraction, leaving taxpayers potentially liable for immense costs, ongoing water treatment, and landscape restoration.” – sourced from Google.

Then there are hundreds of thousands of orphaned gas wells that need to be capped at the taxpayers expense.

“Canada has hundreds of thousands of uncapped, orphaned, and inactive oil and gas wells, primarily in Alberta and Saskatchewan, posing significant risks like methane leaks (seven times higher than reported), water contamination, and land degradation, with costs to plug them estimated in the billions, prompting provincial strategies and federal discussions for cleanup, though current funding often falls short of the massive scale of the problem.“

The point is that Canada only attracts corporations to do business if taxpayers are sponsoring them, and we can no longer afford to that – which is why many are packing up and leaving. This problem, like all of our financial problem is the result of rash and hazardous speculation by both our financial and political environments.

When contemplating how we can arrive at real debt relief one of the first steps is to understand what we debt we have to deal with, and then what resources are available to clean it up. Sadly most Canadians are oblivious to poor state of our country and the need for real action – partly because we are galvanized between left versus right, without noticing the more obvious fact they are both on the same team, and it isn’t ours.

Real Debt Relief.

Real debt relief is only possible for people who are positioned to earn enough, after-tax, money to support a reasonable lifestyle. Unfortunately, the Canadian economy has been in decline for decades mostly driven by debt, and incomes have not kept pace with inflation.

It is extremely challenging for lower income earners to be able to fully extract themselves sufficiently from the necessity of easy access to debt in Canada because incomes are in decline.

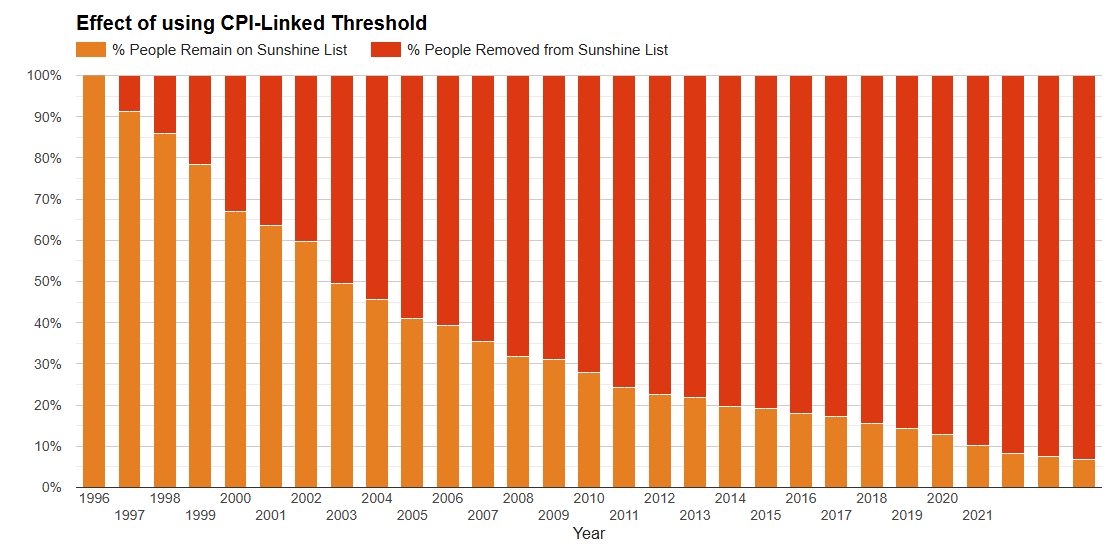

Incomes have been steadily falling, not just nominal incomes but also inflation adjusted incomes have declined significantly. In 1996 the infamous Sunshine List was developed in Ontario. The list still reports people earning a nominal income that exceeds $100,000 – but that 1996 $100,000 is only worth $54,000 today. After properly adjusting for inflation the list should require only people earning about $190,000 be listed.

Poverty has increased exponentially in Canada – with a median pre-tax income of only $42,000, homelessness has increased, foodbank usage has increased, joblessness has increased and the only thing that saves Canadian from being in worse shape than during the Great Depression is DEBT!

- “Overall Increase: Canada’s poverty rate rose for the second consecutive year in 2022, reaching 9.9%, up from 7.4% in 2021 and approaching pre-pandemic levels (10.3% in 2019).

- Children Hit Hard: Child poverty saw its largest recorded annual increase between 2021 and 2022, with rates surpassing pre-pandemic levels by 2022.

- Marginalized Groups Affected More: Racialized populations, Indigenous peoples, immigrants, and people with disabilities consistently experience higher poverty rates, with these gaps widening.” – Sourced from Google.

In 1929, homelessness was not an ongoing social problem, since housing was largely considered a “basic need “that both government and society were obligated to provide. In 2026, homelessness is deeply entrenched, it is a systemic issue caused by chronic affordability crises, and a lack of viable supportive services, rather than a one-time economic event.

According to Statistica, Russia reports about 11,000 homeless people compared with hundreds of thousands in Canada. Even the Canadian government is starting to recognize that a whole industry has been built around maintaining homelessness.

If you cannot afford to live here without using debt simply to survive, how on earth can you ever find real debt relief?

Left versus Right or Up versus Down?

So, real debt relief – really getting out of, and staying out of debt? Don’t hold your breath! You will never see real debt relief until there is a political will to represent the interests of the people over that of the corporatocracy the supports the party system. I shall repeat, because this is important, the notion of left versus right politics is equally a ruse, we need to be concerned more with up versus down than left versus right politics.

Imagine you have$1 million in your estate, while the homeless have nothing at all, when you think about your relative position you are ONE away from the homeless, but compared to the richest man in the world (currently Elon Musk) you are FOUR HUNDRED THOUSAND away from him – yet most people, ironically, find Elon more relatable. Rethink the way you view the world, your neighbours, friends, family, bankers and politicians. And above all rethink what “real debt relief” truly means.

Real Debt Relief will only be possible after we have completely changed our financial systems, and as you can see from the data and the way it has been exploited to the benefit of the very rich, that will not happen as long as “they” are in control, write the rules and have few or no viable consumer protections in place.