Financial Expertise – who can you trust:

Financial expertise and who can you trust to give you sound financial advice in Canada. I did an experiment using the TD Bank, the CMHC and the CRA to assist with calculations. And I am going to preface this blog by saying that the CRA is reportedly providing wrong information 87% of the time, the TD Bank has faced heavy fines for fraud and the CMHC is little more than a slush fund for bankers.

Having said that the TD bank and the CRA came far ahead of CMHC in terms of utility – so what did I do?

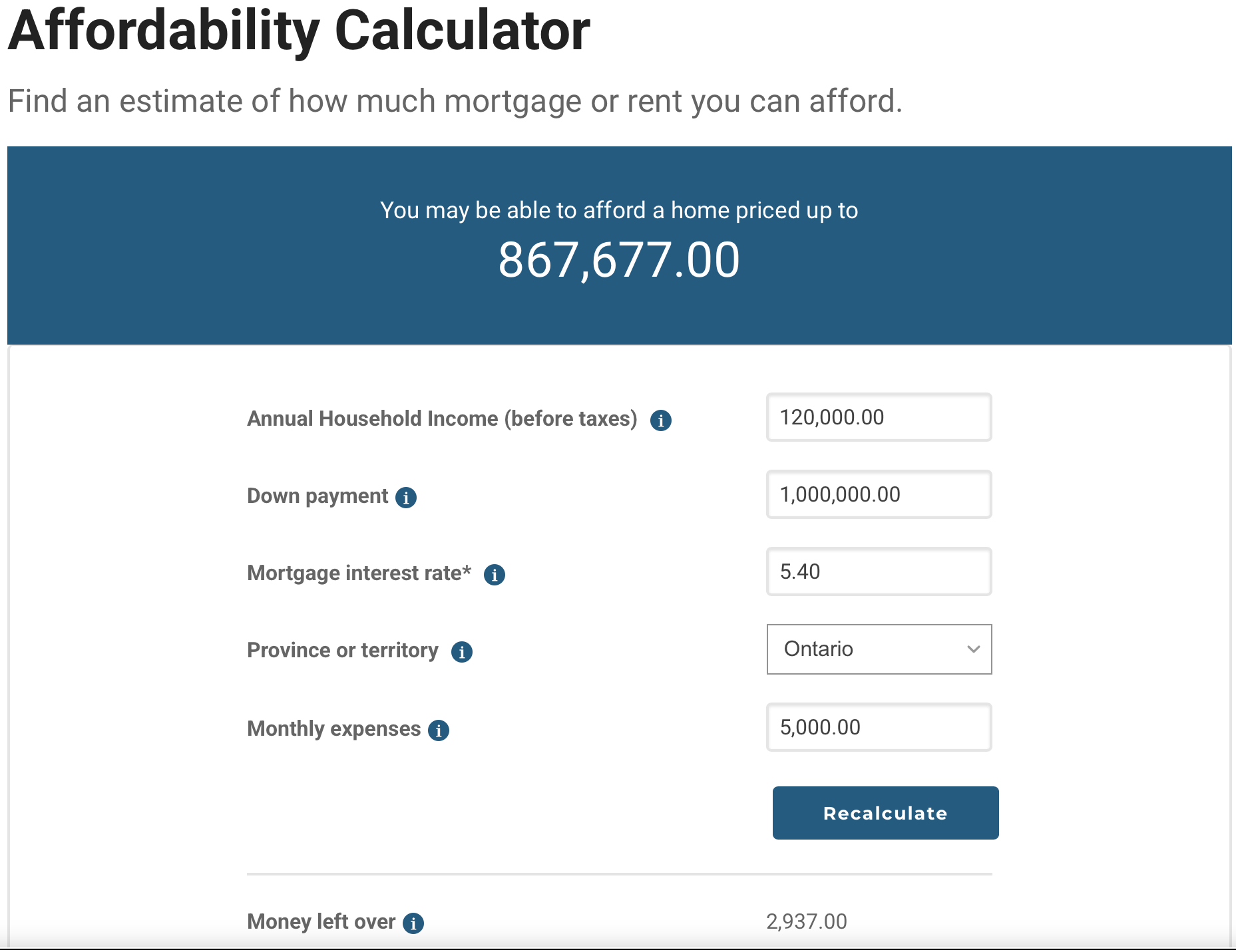

I started by asking the CMHC about housing affordability – my assumption we have a couple with four children, they are each slightly better than average income earners earning $120,000 per year $60,000 each). Going a step further, I assumed that grandma had died and left them $1,000,000 in cash to use towards buying a home.

I assumed they would be seeking a mortgage at 5.4% – a typical rate in today’s market and they live in Ontario. I used the CRA payroll calculator to estimate their monthly take home income – $7,890 between them. CMHC asked what their monthly expenses, excluding housing were, I suggested $5,000 CMHC calculated they would have some $2,937 left for housing costs – pretty close.

The genius level calculator at CMHC determined they could afford to buy a house for $867,677 – site I had indicated they had a million dollar downpayment I made the critical decision that the CMHC meant they could afford a mortgage of that amount. So, I took that number and plugged it into TD Bank’s mortgage payment calculator – which does provide reliable estimates.

The TD mortgage payment calculator, using the value provided by CMHC (a crown corporation) with interest calculated at 5.4%, reported the monthly payments would be $5,246 – just for the mortgage – no property taxes, no home owner insurance and no utilities or maintenance.

Clearly this is ridiculous, bad advice and completely misleading information. The CMHC’s prime objective has long been to prop up the banks, the banks to drive you into debt and the CRA to collect as much money from you as they can.

When you are looking for financial expertise – you have to look long and hard to find good quality, reliable information. Realtors are trained in a few months, mortgage agents in a few days, CRA operatives have no accounting background, your investment adviser is schooled in regulations not investing, leaving you and your money blowing in the wind.

In Canada white collar crime is common and the penalties are so light they are seen as the cost of doing business. The person most likely to defraud you is the person who keeps you in a positive feedback loop, never seems disagreeable, always telling you what you want to hear.

Economically, Canada is a dumpster fire in need of a systemic paradigm shift to rebalance the economy – taxes, all taxes, erode some 43% of our gross income, servicing debt (not paying it down or off) costs 42% of our gross income. Debt has become so ubiquitous than people are lost, and have no one to turn to for sound financial expertise and advice to help them negotiate the complexities of the pickpockets.